CSRD & ESRS

CSRD: The Corporate Sustainability Reporting Directive

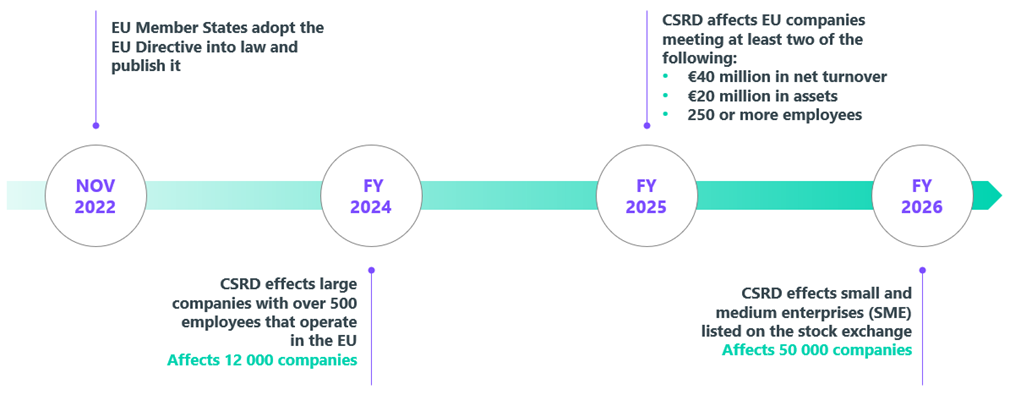

The CSRD represents a significant advancement in sustainability reporting across the European Union. Officially coming into force on January 5, 2023, the reporting standard mandates comprehensive, consistent, and standardized reporting of ESG activities by companies within the 27 EU member states. The directive is being implemented progressively, starting with large companies and gradually including smaller enterprises, providing SMEs with additional time to prepare and comply with the new regulations.

Key Aspects of the CSRD:

- Standardization of Reports: The CSRD aims to normalize how companies report on their sustainability activities, ensuring that ESG reporting is as routine and standardized as financial reporting.

- Phased Implementation: This staggered approach helps ensure that all companies, regardless of size, have adequate resources and time to meet the reporting standards set forth by the CSRD.

ESRS: European Sustainability Reporting Standards

Developed by the European Financial Reporting Advisory Group, the ESRS provide a detailed framework and methodology for reporting on ESG metrics. The standards are designed to enhance the relevance, comparability, and reliability of sustainability information.

Double Materiality Perspective:

The ESRS adopt a double materiality perspective, which requires companies to report on:

- Impact Materiality: How the company's operations impact the environment and society.

- Financial Materiality: How environmental and social issues affect the company's financial performance.

Key Components of the ESRS:

ESRS 1 (“General Requirements”) sets general principles to be applied when reporting according to ESRS and does not itself set specific disclosure requirements. ESRS 2 (“General Disclosures”) specifies essential information to be disclosed irrespective of which sustainability matter is being considered. All the other standards and the individual disclosure requirements and datapoints within them are subject to a materiality assessment. The ESRS include 85 disclosure requirements with more than 1100 data points in 12 standards.

Scope and Implementation of CSRD and ESRS

Whole Value Chain Disclosure:

Organizations are required to disclose information relevant to their entire value chain. This comprehensive approach necessitates collaboration with suppliers and business partners to gather necessary data, particularly challenging for small companies that must secure access to this information in preparation for their own reporting obligations.

Double Materiality Assessment:

This assessment is crucial for determining the relevance of information, focusing on:

- Company Impact on Sustainability: Evaluating how the company's activities influence environmental and social factors.

- Sustainability Impact on Company: Assessing how environmental and social challenges could pose financial risks or opportunities for the business.

Legal Binding Nature:

Both the CSRD and the ESRS are legally binding, meaning that compliance is not optional. Companies within their scope are required to integrate these standards into their annual reporting processes, subject to legal enforcement and potential penalties for non-compliance.

Conclusion

The CSRD and the ESRS mark a pivotal shift towards more transparent, consistent, and comparable sustainability reporting within the EU. By adhering to these standards, companies not only comply with legal requirements but also contribute to a more sustainable global economy, aligning their operations with broader societal goals. The phased implementation of these directives ensures that businesses have the necessary framework and time to adapt, ultimately fostering a more sustainable approach to corporate governance and operations.